Banking fraud no longer looks like a stolen card. It looks like a deepfake video call from your “CFO.” It looks like a synthetic identity built in minutes. AI in FinTech has become the only real answer to threats moving this fast.

In 2026, fraud is not seasonal. It is continuous, automated, and adaptive. The World Economic Forum projects AI-enabled cybercrime could cross $10 trillion annually by 2030. Banks that still rely on static rules are already behind. This blog breaks down how modern AI fraud detection systems work, what technology powers them, and why Ahmedabad’s engineering talent is quietly becoming a global banking security asset.

Key Takeaways

- AI in FinTech now drives real-time fraud prevention, not just detection.

- Traditional rule-based systems miss new fraud patterns constantly.

- Anomaly detection algorithms learn normal behavior, then flag deviations instantly.

- Behavioral analytics catches account takeover even with correct passwords.

- Deepfake fraud caused a confirmed $25 million corporate loss in 2026.

- 60% of banks lack a plan for agentic AI fraud.

- AmEx and PayPal each improved detection accuracy using AI models.

- VectovateAI delivers 40% higher fraud detection accuracy for finance clients.

- Explainable, low-latency fraud detection models are now a compliance requirement.

Why is AI Fraud Detection Critical for Modern Banking Systems?

Traditional fraud tools were built for a slower world. They flagged transactions using fixed thresholds. If a withdrawal crossed a limit, the system blocked it. This approach worked when fraud moved slowly. It fails against today’s fraud.

Fraudsters now use generative AI too. They create synthetic identities in seconds. They clone voices from ten-second audio clips. A JPMorgan Payments report found humans correctly spot deepfake videos just 40% of the time. Over half of the people surveyed have faced a deepfake-driven scam attempt.

This is why banks need an AI fraud detection system, not a rulebook. AI doesn’t wait for a known pattern to reappear. It learns what “normal” looks like for every single user. Then it flags anything that breaks that pattern instantly.

The stakes are also regulatory, not just financial. Banks must maintain compliance under PCI DSS, GDPR, and RBI norms. A single missed fraud event can trigger heavy penalties. It can also destroy years of customer trust. AI fraud detection protects revenue, reputation, and regulatory standing together.

AI fraud detection powers real-world banking use cases:

Fraud detection models now protect banks at every touchpoint. From card transactions to loan applications, AI flags risk instantly.

Here are the use cases delivering real, measurable impact

How Does Machine Learning Fraud Prevention Actually Work?

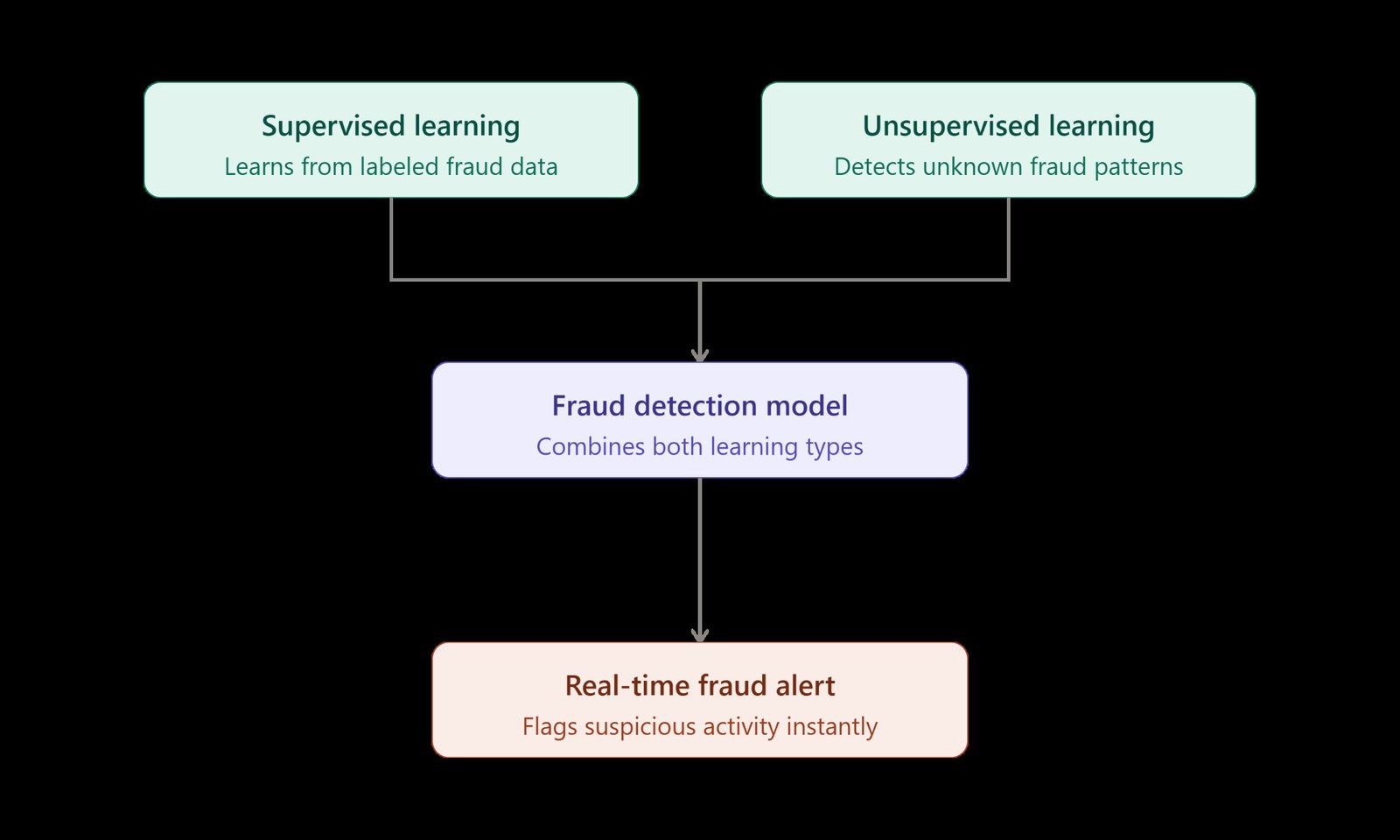

Machine learning fraud prevention relies on two core training methods, as outlined by IBM’s research on AI in banking. Each method solves a different piece of the puzzle.

Supervised learning trains models on labeled historical data. Analysts feed the system thousands of past transactions. Some are legitimate, others are confirmed fraud. The model learns to separate the two categories. Over time, it recognizes known fraud signatures instantly.

Unsupervised learning works differently, and it matters more. It doesn’t need labeled fraud examples to function. Instead, it studies typical account behavior continuously. When something deviates from that baseline, it flags it. This is how banks catch fraud tactics nobody has seen before.

Together, these methods create a fraud detection model that keeps improving. It doesn’t just catch old fraud patterns. It anticipates new ones before they spread across accounts.

Here’s a diagram showing how the two core methods combine into a working fraud detection model:

The Technology Stack Behind Real-Time Fraud Monitoring

Real-time fraud monitoring depends on several AI components working together. Here’s how each piece contributes to the system.

| Technology | Function | Banking Impact |

|---|---|---|

| Anomaly detection algorithm | Flags deviations from a user’s normal behavior | Catches unknown fraud patterns instantly |

| Behavioral biometrics | Analyzes typing speed, cursor movement, and login rhythm | Detects account takeover before login completes |

| Graph neural networks | Maps relationships between accounts and transactions | Uncovers organized fraud rings and money laundering |

| Natural language processing | Reads chat, email, and voice interactions | Flags social engineering and phishing attempts |

| Computer vision | Verifies KYC documents and biometric ID | Speeds onboarding and blocks fake identities |

| Risk scoring engines | Weighs transaction amount, location, and frequency | Assigns real-time risk scores per transaction |

Each layer adds a different signal. Combined, they build a pattern recognition fraud framework far stronger than any single tool. This is the technical backbone modern banks now depend on.

Behavioral Analytics: The Quiet Game-Changer

Behavioral analytics is arguably the biggest shift in banking security. It doesn’t just watch transactions anymore. It watches how a person actually behaves.

Every user has a rhythm. They log in at certain hours. They type at a certain speed. They hold their phone at a certain angle during scrolling. AI models learn these micro-patterns silently over time.

When a fraudster steals valid login credentials, their behavior still differs. Their typing cadence is different. Their navigation flow feels unfamiliar to the model. Behavioral analytics catches this mismatch even when passwords are correct.

This approach also reduces false positives significantly. A customer making an unusually large purchase isn’t blocked instantly. The system checks their broader behavioral context first. This keeps legitimate customers moving without unnecessary friction.

Traditional vs. AI-Powered Fraud Detection: A Clear Comparison

Banks often ask why legacy systems can’t simply be upgraded. The table below explains the real gap.

| Factor | Traditional Rule-Based Systems | AI-Powered Fraud Detection |

|---|---|---|

| Detection method | Fixed thresholds and static rules | Continuous behavioral and pattern learning |

| Speed | Batch processing, delayed alerts | Real-time fraud monitoring, instant flags |

| False positives | High, causing customer friction | Lower, due to contextual scoring |

| Adaptability | Requires manual rule updates | Learns and adapts automatically |

| Scale | Struggles with rising transaction volume | Processes millions of events per second |

| New fraud tactics | Often missed until reported | Caught through the anomaly detection algorithm signals |

The difference isn’t incremental. It’s structural. AI systems don’t just detect fraud faster. They understand that context traditional systems were never built to read.

Proof It Works: Real Numbers From the Industry

Skeptical banking leaders often want evidence, not theory. The results already speak clearly.

American Express improved fraud detection accuracy by 6% using LSTM-based AI models, per IBM’s analysis. PayPal improved real-time fraud detection by 10% through continuous AI monitoring, as reported by IBM. VectovateAI’s own finance-sector engagements report a 40% increase in fraud detection accuracy using behavioral biometrics. Claims automation projects reduced operational costs by 65% for insurance partners.

These aren’t marginal gains. In banking, a 6-10% detection improvement prevents millions in annual losses. It also protects thousands of customer accounts from compromise.

2026’s Biggest Threat: Deepfakes and Agentic Fraud

This year introduced a new fraud category entirely. Deepfake-driven payment fraud is now a boardroom-level risk.

A multinational company lost $25 million after an employee trusted a deepfake CFO video call. The instructions seemed legitimate. The face and voice matched perfectly. No system was hacked; only human trust was exploited.

Accenture’s 2026 banking research found 60% of financial institutions lack a dedicated response plan for agent-driven fraud. Yet 57% of banking IT executives expect AI agents to be fully embedded in fraud detection within three years. The gap between threat and readiness is closing slowly.

Defending against this requires layered security, not one tool. Behavioral analytics catches unusual context around a request. Real-time validation checks payment details against authoritative sources. Zero-trust identity frameworks verify every request, every time, without exception.

Building a Fraud Detection Model That Actually Scales

Banks evaluating AI vendors should prioritize four capabilities. These separate genuine platforms from surface-level dashboards.

- Governed data pipelines: Sensitive fields must be tokenized before reaching any model.

- Continuous learning: The fraud detection model must adapt without manual retraining cycles.

- Explainability: Regulators require clear reasoning behind every fraud flag issued.

- Low-latency scoring: Real-time fraud monitoring only works below 200-millisecond response times.

Skipping any of these creates hidden risk. A model without governance leaks sensitive data. A model without explainability fails audits immediately. Banks need partners who understand both the AI and the compliance layer.

VectovateAI, Fintech App Development Services

This is exactly where VectovateAI fits into the picture. Based in Ahmedabad, we build AI-native fintech and banking platforms for global clients. Our approach isn’t AI-for-hype; it’s agent-first, human-in-the-loop engineering.

We deliver real-time fraud prevention using behavioral biometrics, not static rule engines. Our credit risk assessment tools analyze transaction history and behavior instantly. Our platforms use AES-256 encryption and zero-trust architecture by design. Every solution stays compliant with SEC, FINRA, GDPR, and PCI DSS standards.

Our finance and insurance engagements have delivered measurable results already. A 40% increase in fraud detection accuracy for banking partners. A 90% faster underwriting turnaround using NLP and OCR automation. A 65% reduction in claims processing costs for insurance clients.

Ahmedabad’s engineering talent brings a specific advantage most agencies lack. Deep technical depth, paired with genuine cost efficiency at scale. We don’t just deploy AI models; we govern them responsibly.

If your bank or fintech platform needs a modern AI fraud detection system, our team can architect it end-to-end. From behavioral analytics to real-time monitoring dashboards, we build it all in-house.

Final Thought: Security Is Now a Product Feature

Fraud detection in 2026 isn’t a back-office function anymore. It’s a core product experience customers directly feel.

Slow, rigid systems frustrate legitimate users constantly. Smart, adaptive systems protect users invisibly, without friction. Banks that invest in real AI infrastructure now will lead. Those relying on legacy rule engines will keep losing ground.

The technology exists today, tested and proven at scale. The question is which banking partner builds it right.

Leave a Reply